PRMIA 8006 (PRM Exam I) Overview -- 2015 Edition

So here's the deal: if you're eyeballing the PRMIA 8006 Exam I, you're basically staring down the first real hurdle in the Professional Risk Manager certification track. This isn't some weekend quiz. It's the foundational gateway testing whether you actually get finance theory, financial instruments, and how markets really operate. The 2015 Edition specifically captures a post-crisis world where regulators and employers got dead serious about risk management competency.

The exam doesn't mess around, honestly. It validates you can handle time value of money calculations, portfolio theory, asset pricing models, derivatives mechanics, and market microstructure. Not just memorize formulas, but actually apply them when someone throws a bond pricing problem or an options hedge scenario your way. You'll need to demonstrate understanding of why certain pricing relationships hold, not just plug numbers into calculators.

Who's actually taking this thing

The target audience? Pretty broad, I mean. Aspiring risk managers obviously, but also financial analysts wanting to pivot into risk roles. Treasury professionals show up constantly. Compliance officers trying to beef up technical chops. Recent finance graduates who realize a degree alone doesn't cut it anymore in competitive job markets. I've even seen a few auditors who got tired of just checking boxes and wanted to understand what the numbers actually meant.

Career-wise? Passing the full PRM opens doors to market risk analyst positions, credit risk officer roles, operational risk specialist gigs, portfolio risk manager tracks, even enterprise risk consultant positions. The PRMIA 8006 is your first step toward those titles, and employers recognize the certification because it signals standardized knowledge rather than whatever random mix of skills you picked up at your last company.

What makes this exam different from other certs

Unlike the FRM or CFA, the PRM certification path focuses exclusively on risk management applications. You're not learning portfolio construction for alpha generation. You're learning how to measure, monitor, and manage risk exposures.

The breadth? Real. Equities, fixed income, derivatives, alternative instruments all get covered, but always through the lens of risk-return relationships and pricing fundamentals. The 2015 Edition specifically incorporates lessons from the 2008 financial crisis. Liquidity risk, counterparty risk, systemic market failures aren't theoretical anymore. The exam expects you to understand how OTC markets seized up, why credit derivatives amplified losses, and what role market microstructure played in cascading failures.

The actual content you're dealing with

Finance theory foundations eat up a big chunk. Present value calculations, bond duration and convexity, yield curve analysis. You need computational skills here, not just conceptual handwaving. Can't calculate the price of a bond given spot rates? You're gonna struggle.

Derivatives pricing is unavoidable. Binomial models for options, Black-Scholes framework basics, put-call parity, replication strategies. The thing is, the exam wants to see you understand how arbitrageurs enforce pricing relationships and why certain derivative payoffs exist. Honestly the relationship between spot and forward/futures prices across different asset classes trips people up more than it should.

Market structure questions test whether you understand bid-ask spreads, price discovery mechanisms, how different market participants interact. Not super deep, but you need to know why securities trade at premiums or discounts and what drives transaction costs.

Study commitment and difficulty

Plan on 150-200 hours depending on background. Got an undergrad finance degree and some market experience? Maybe closer to 150. Coming from a non-finance role? Budget 200+ and don't skimp on fundamentals.

Difficulty level? Challenging but achievable. PRMIA designs this for candidates with undergraduate finance education plus focused prep. It's harder than most single-topic certs but not as brutal as actuarial exams. The multi-step calculations and scenario interpretation questions separate people who memorized formulas from those who actually grasp the material.

How this fits into the bigger PRM picture

The PRMIA 8006 exam is prerequisite knowledge for everything that comes after. Exam II dives into mathematical foundations of risk measurement: VaR, expected shortfall, correlation modeling. You can't handle that without nailing the finance theory tested in Exam I.

Exam III covers risk management practices across market risk, credit risk, operational risk. Again, you need the instrument knowledge and pricing fundamentals from Exam I. Exam IV hits case studies, standards, governance, ethics. Practical application of everything prior.

Not gonna lie, some people underestimate Exam I because it's "just foundations." That's a mistake. The subsequent exams build directly on this material. If you barely scrape by on Exam I, you'll suffer later.

What successful candidates can actually do

After passing, you should be able to read financial market data without confusion, understand instrument documentation, assess basic risks embedded in positions, and communicate findings using standard terminology. You gain fluency in the language of financial markets. Critical when you're talking to traders, portfolio managers, or presenting to senior risk committees.

The exam emphasizes understanding how financial instruments transfer risk between participants and how markets aggregate information into prices. These aren't just academic concepts. In a real risk management role, you need to explain to someone why a particular hedge makes sense or why certain positions create unexpected correlation exposures.

Exam mechanics worth knowing

Mixed feelings here. The PRMIA 8006 exam cost varies by membership status and geography, but budget several hundred dollars. PRMIA members get discounts. The PRMIA 8006 passing score isn't publicly disclosed as a fixed number. PRMIA uses scaled scoring and adjusts for difficulty. Generally you're looking at needing 60-70% correct, but don't quote me since the organization doesn't publish exact cutoffs.

Question style mixes calculations, interpretations, scenario analysis, and conceptual understanding. Some questions require multi-step work. Others test whether you can identify arbitrage opportunities or apply hedging strategies. The exam doesn't give partial credit, so wrong calculations mean wrong answers.

Study materials and prep strategy

Official PRMIA readings? Your foundation. They're full but dense. Most candidates supplement with third-party study notes that break down complex topics.

PRMIA 8006 practice tests are critical. You need to experience the question style and timing pressure. Official mocks are best if available, but third-party practice tests help too.

High-impact topics to prioritize: bond math like duration, convexity, and yield measures. Derivatives pricing including binomial trees and Black-Scholes basics. No-arbitrage conditions. Forward pricing relationships. These show up repeatedly and connect to multiple other topics.

Common mistakes? Rushing calculations. Confusing similar formulas (modified duration vs Macaulay duration gets everyone). Not reading questions carefully. The exam loves to test edge cases and scenarios where intuition might mislead you.

Why this certification still matters

The 2015 Edition content remains relevant because fundamental finance theory doesn't age. Arbitrage pricing, risk-neutral valuation, no-arbitrage conditions provide timeless frameworks. Markets evolve, instruments get more complex, but the underlying principles tested in PRMIA Exam I stay foundational.

Professional benefits include enhanced credibility, systematic knowledge organization, and competitive advantage in risk management job markets. The certification signals you've met international standards rather than just learned whatever your employer happened to teach you.

For anyone serious about a risk management career, PRMIA 8006 represents the starting line. Not the finish line, not even close. But you can't advance to mathematical risk measurement or enterprise risk frameworks without proving you understand how financial markets actually function at a fundamental level. That's what this exam tests, and that's why it matters.

PRMIA 8006 Exam Objectives and Content Domains

What PRMIA 8006 Exam I is really testing (2015 Edition)

Okay, so PRMIA 8006 Exam I (the 2015 Edition) is the "do you actually speak finance or are you just nodding along" checkpoint in the PRM program. It's not transforming you into some quant wizard or day trader overnight. What it does is check if you can look at a risk report, figure out what instrument they're talking about, and crank through the basic math quickly enough that you don't completely freeze when the question suddenly jumps from a bond to an option to some market microstructure curveball.

The Professional Risk Manager Exam I syllabus breaks down into three content domains. PRM Exam I Finance Theory sits around 35 to 40%, PRMIA Exam I Financial Instruments takes up roughly 40 to 45%, and PRMIA Exam I Financial Markets grabs about 20 to 25%. That weighting? It matters. People love studying whatever feels intellectually impressive and then get absolutely demolished by the sections they thought were boring. Short sentences here. Formulas everywhere. Tons of them.

The thing is, this exam's old enough (2015 Edition) that some of the post-crisis regulation references feel dated in tone, but the core mechanics stay evergreen. And the stuff that never changes is what they test the hardest anyway. I've seen candidates spend three weeks perfecting exotic option theory while totally ignoring how to price a plain vanilla bond, which is insane when you think about how the actual weighting works.

Who should take it, and why you'd bother

If you're working in risk, treasury, trading support, model validation, investment operations, or even audit, this exam forces you to stop casually tossing around terms like duration, carry, beta, and clearing. You actually have to compute them and explain them when you're under pressure and everyone's watching. Hiring managers don't always obsess over whether you know some niche pricing trick. They care that you won't misread a yield quote or mix up forward against futures mechanics when the PnL's swinging and the room's tense.

Career-wise? Look, PRM certification Exam I objectives align with entry to mid-level risk analyst roles, and it's a solid signal if you're pivoting from general finance into market risk or product control. Not magic. Still useful.

Finance theory foundations you'll see everywhere (35 to 40%)

This section? People underestimate it because it sounds like undergrad finance. The exam doesn't care about your confidence. It wants correct outputs.

Time value of money is the computational foundation. Present value and future value show up directly, but they also sneak into bond pricing, swap valuation intuition, and even option tree discounting. Expect annuities and perpetuities. Don't be shocked by continuous compounding showing up. One clean mental model helps: discrete compounding is "stepwise growth," continuous compounding is "always on," and you've gotta move between discount factors, rates, and cashflow timing without pausing to re-derive everything from scratch.

Mean-variance portfolio theory's another big chunk: expected returns, variance, covariance, and how you interpret correlation. Diversification benefits aren't just a slogan. You need to actually compute portfolio variance, recognize when correlation drives risk reduction, and understand the efficient frontier conceptually, even if the exam keeps the math reasonable. You'll also see risk-adjusted performance ideas like Sharpe ratios and information ratios. You must distinguish expected return (what you think will happen) against realized return (what actually happened). Sounds obvious, right? People still blow it.

CAPM's the classic equilibrium pricing model they love because it's got clean conceptual hooks: systematic against idiosyncratic risk, beta as sensitivity to the market factor, and the security market line. You should know what assumptions make CAPM "work" in theory, and why those assumptions are questionable in real markets. Some questions are basically "which assumption's being violated here?" Not gonna lie, CAPM questions can feel like vocab tests until you grind enough practice and realize they're checking whether you can reason from the model, not worship it.

APT takes CAPM's single factor and says "markets probably price multiple sources of risk." You'll be expected to understand factor exposures, factor risk premia, and the arbitrage argument that forces pricing relationships to hold, at least approximately. The math's usually linear and readable. The trick is interpretation: which factor's being priced, what is exposure, and what does mispricing actually imply.

Market efficiency and behavioral finance are the "humans are messy" portion. Weak-form, semi-strong-form, strong-form efficiency, plus what each implies for technical analysis and fundamental analysis. Then behavioral biases like overconfidence, anchoring, and herding, and how those can create anomalies that look like free money until they aren't. Fragment here. "Markets are rational" isn't the point. The point's knowing what each framework predicts.

Financial instruments you must know cold (40 to 45%)

This is the heaviest domain, and it's the one that separates "I read the chapter" from "I can answer under time pressure." PRMIA Exam I Financial Instruments covers cash products and derivatives across rates, credit, equity, FX, and commodities.

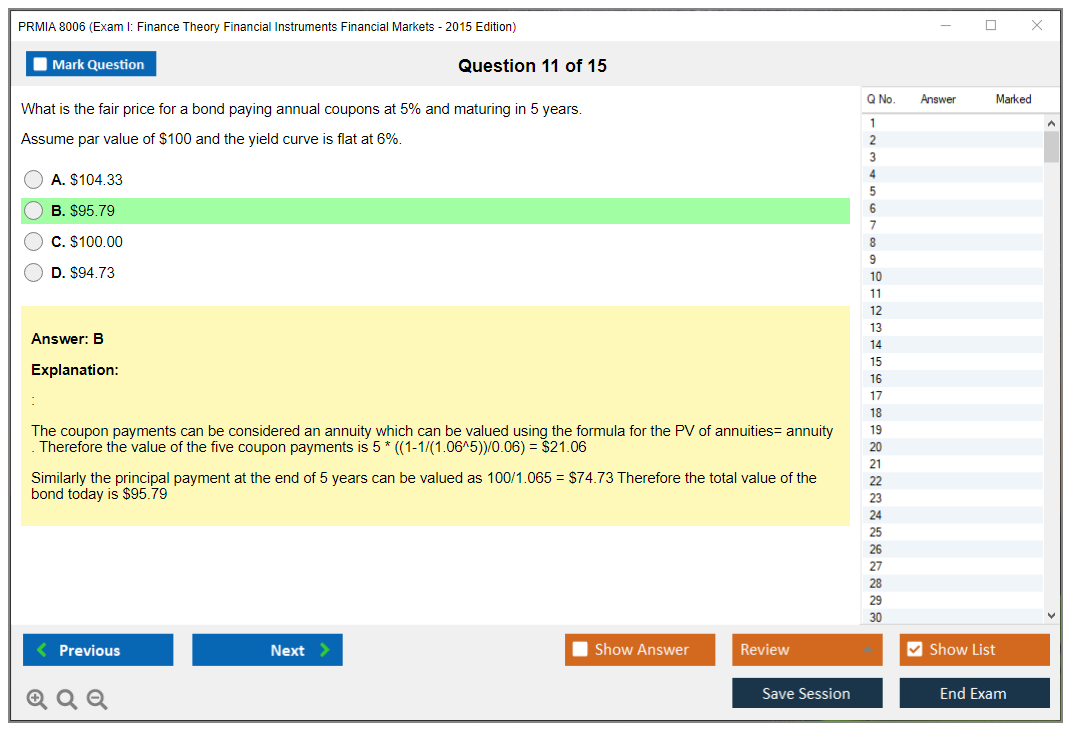

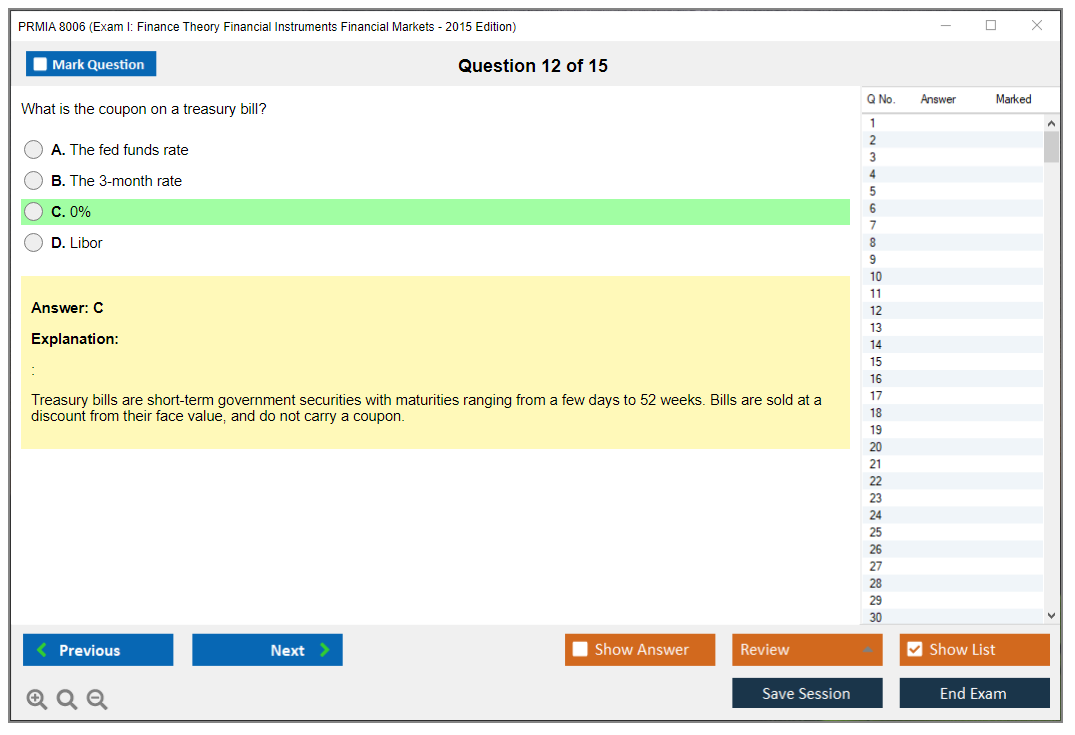

Fixed income's core: government bonds, corporates, municipals, mortgage-backed securities, and asset-backed securities, with a focus on cashflow structure. You need to be comfortable with coupon schedules, pricing off spot rates and forward rates, yield to maturity and par yields, and the basic price-yield relationship (yields up, prices down). The exam will definitely ask you to price a bond using a curve. If you only memorized YTM tricks, you're gonna feel it.

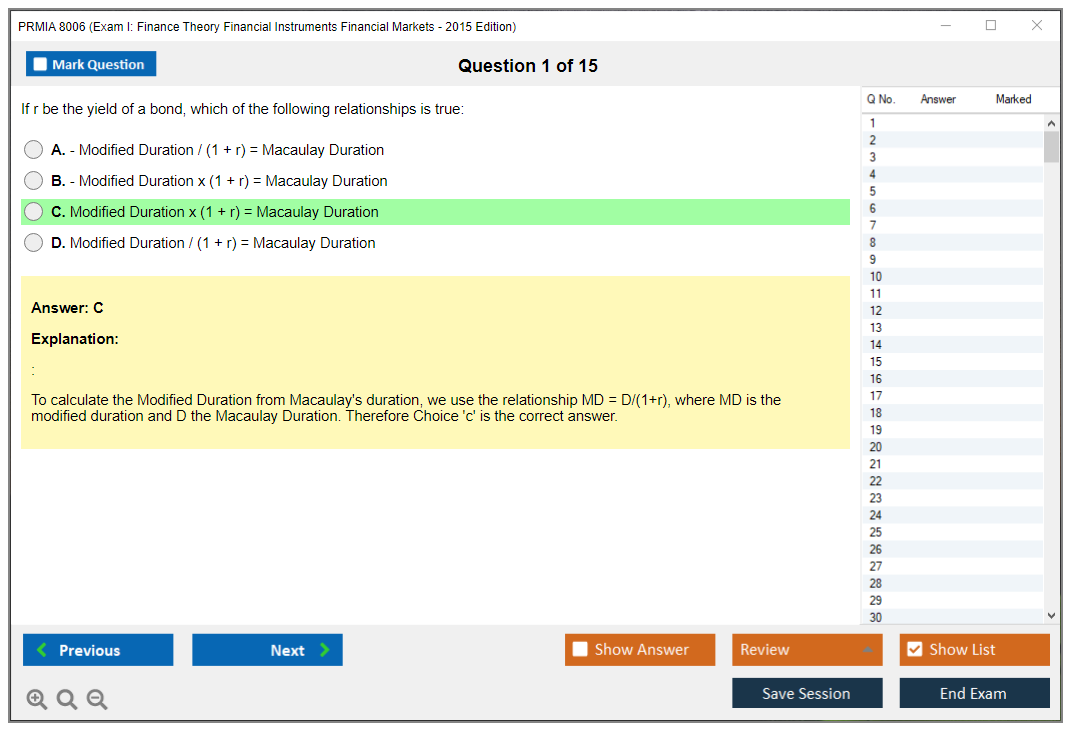

Duration and convexity are the sensitivity toolkit. Macaulay duration against modified duration, and why modified duration maps more directly to price change for a yield move. Effective duration comes in when cashflows change with rates (hello MBS). Convexity's the second-order adjustment that makes your "duration estimate" less wrong for larger yield moves. Here's my take: if you can explain duration in plain English and still do the math, you're ahead, because most candidates can only do one of those things.

Equity instruments? Broader than "common stock." Preferred stock, convertibles, warrants, rights, and basic valuation approaches. The exam tends to focus on payoff characteristics and risk features rather than making you run a full DCF. Still, understand what optionality exists in convertibles and warrants, because that optionality connects directly to options intuition.

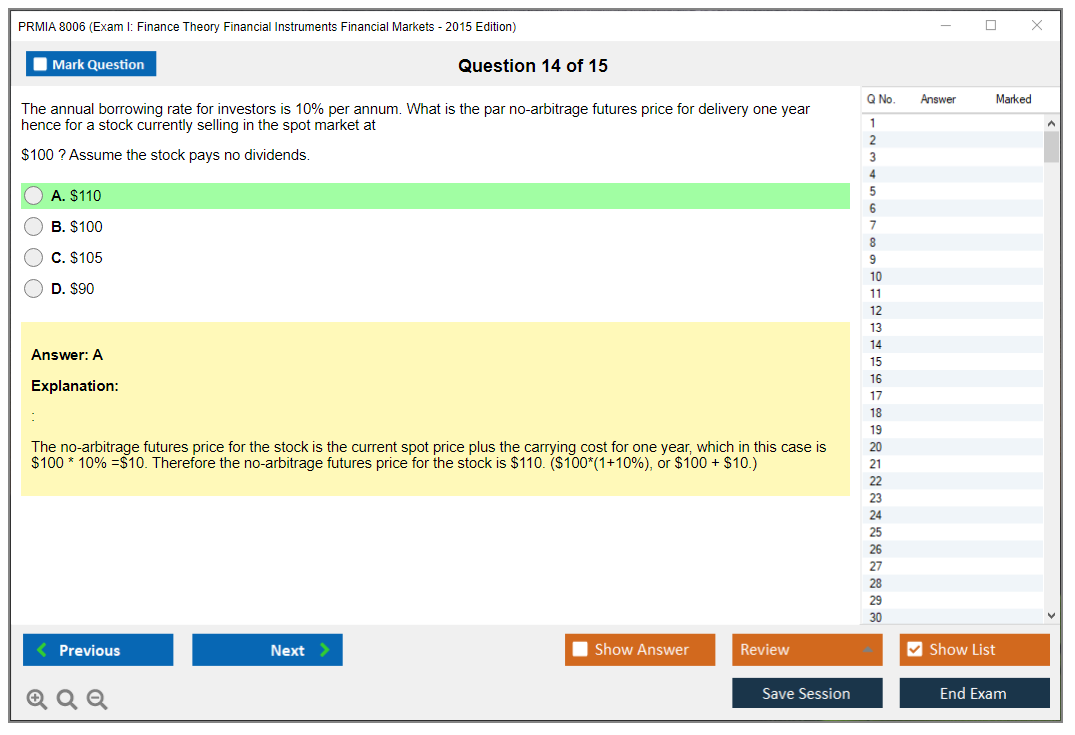

Derivatives are where candidates either thrive or spiral. Forwards: cost-of-carry pricing, basis risk, and hedging applications in commodities, currencies, and rates. Futures: margin, marking-to-market, convergence to spot at expiration, and what's operationally different from a forward. The mechanics matter. Daily settlement changes credit exposure. That's the point.

Options fundamentals? Non-negotiable stuff here: call and put payoffs, intrinsic against time value, moneyness, American against European exercise, and basic strategies. Then option pricing via binomial trees, one-period and multi-period, risk-neutral valuation, replication, and delta hedging as the intuition bridge between "model" and "risk management." After that comes Black-Scholes-Merton for European options: formula components, assumptions, and the Greeks (delta, gamma, vega, theta, rho). Model limitations show up too, usually as "what assumption is unrealistic" or "what risk isn't captured."

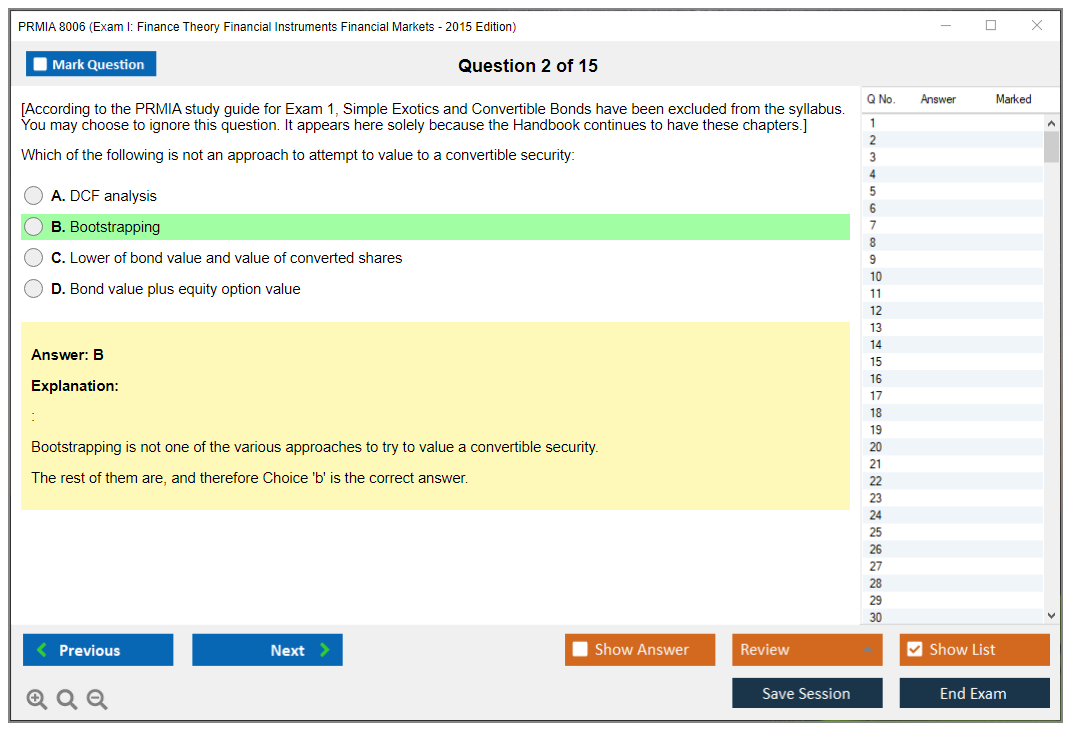

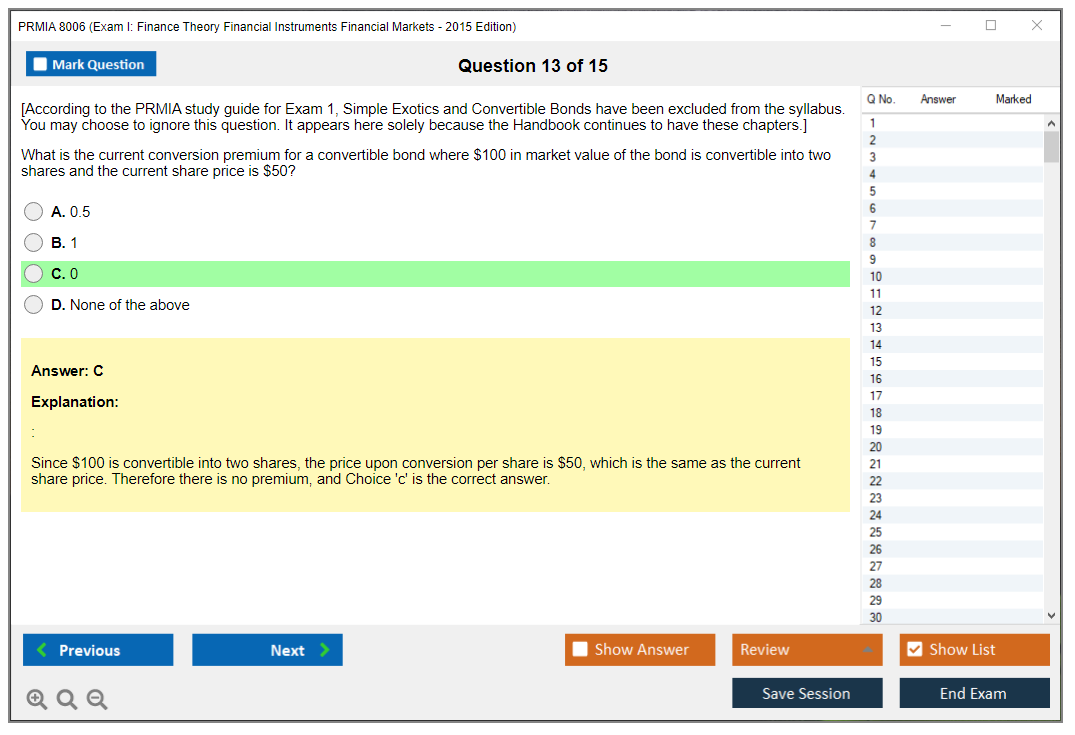

Swaps mean interest rate swaps, currency swaps, commodity swaps. Pricing at inception's usually "set fixed rate so PV fixed leg equals PV floating leg." Valuation during the life is about discounting remaining cashflows and recognizing counterparty risk. Credit derivatives include CDS, total return swaps, and credit-linked notes. You should know reference entity, credit events, and how protection works. Exotic derivatives like barrier options, Asian options, and compound options are typically more conceptual, with path-dependency and payoff shape as the key idea.

Financial markets and how prices actually form (20 to 25%)

PRMIA Exam I Financial Markets is the smaller weight, but it's where the exam checks whether you understand trading reality, not just textbook pricing.

Market microstructure: bid-ask spreads, order types (market, limit, stop), order books, and why liquidity providers earn the spread while taking inventory and adverse selection risk. Exchange-traded against OTC's a recurring theme: standardization, clearing, transparency, and counterparty risk differences. Clearing and settlement basics matter too, including CCP clearing, netting, collateral, and settlement risk. Short sentence. This is plumbing. Plumbing breaks careers.

Participants show up in lots of scenarios: hedgers, speculators, arbitrageurs, market makers, and what each is trying to accomplish. Primary markets cover IPOs, seasoned offerings, bond issuance, underwriting and bookbuilding. Secondary markets cover continuous trading, auctions, transparency, and liquidity drivers.

Regulation's in scope at a high level, including post-crisis reforms like Dodd-Frank and EMIR, capital requirements, and derivatives oversight. You're not writing a legal memo. You're recognizing what regulation changed about clearing, reporting, and counterparty risk.

Indices and market benchmarks matter too: price-weighted against value-weighted against equal-weighted construction and what that implies for performance interpretation. FX markets show up with spot, forwards, swaps, quotation conventions, and triangular arbitrage. Commodity markets bring storage costs, convenience yield, and backwardation against contango. Money markets include T-bills, commercial paper, CDs, and repos.

The integrated questions are the real exam

The sneaky part of PRMIA 8006 Exam I 2015 Edition is the applied integration. You'll get questions that combine theory plus instrument plus market mechanics, like using cost-of-carry in a commodity forward while reasoning about contango, or pricing a bond with spot rates and then interpreting duration risk after a yield shift, or linking CAPM beta intuition to an equity derivative hedge. That's why a PRMIA 8006 question bank and timed practice matter way more than rereading notes.

Cost, passing score, difficulty, and study resources (quick reality check)

People ask about PRMIA 8006 exam cost and PRMIA 8006 passing score constantly. PRMIA's pricing and policies can shift by region and testing window, so you've gotta confirm in the PRMIA portal. Plan for exam fees plus any enrollment or membership-related charges depending on how you register. Passing score isn't usually framed as a simple fixed percentage you can game. Honestly that's fine, because the way to "pass" is competence across domains, not perfection in one.

On PRM Exam I difficulty level, it's different from FRM/CFA. It's less about marathon reading and more about being sharp on core mechanics across many products, with enough math to punish sloppy setup. If you're solid on fundamentals and you practice? It's fair. If you avoid calculations, it's brutal.

For PRMIA Exam I study materials, start with official readings, then add a focused set of notes or a prep book that matches your gaps. For PRMIA 8006 practice tests, use timed mocks, keep an error log, and redo missed questions until the steps feel automatic. Mentioning the rest: formula sheets, flashcards, and a small set of "redo" problems help more than collecting five different prep courses.

Renewal basics, since people forget this exists

PRMIA recertification and renewal requirements are part of the bigger PRM program expectations, usually tied to continuing professional development and periodic reporting. Don't treat it as paperwork later. Track learning hours as you go, keep proof, and you won't hate your future self during audit season.

PRMIA 8006 Exam Format, Passing Score, and Difficulty Level

Look, if you're serious about getting your Professional Risk Manager credential, you need to actually understand the PRMIA 8006 Exam I format and what passing requires. I've watched too many candidates dive straight into study guides without grasping the basic structure of this thing, which is just backwards.

The PRMIA 8006 passing score isn't published as a fixed percentage, which frustrates people. PRMIA uses criterion-referenced scoring. Translation? You're measured against a competency standard, not other test-takers. The association brings in subject matter experts who determine what minimum knowledge someone needs to function as a competent risk professional, then sets the bar there. You can't game this hoping everyone bombs. Either you know the material or you don't.

What you're actually facing on exam day

The examination's entirely multiple-choice. No essays. No case studies requiring paragraph responses. Just questions with four or five answer choices, one correct, the rest designed to catch partial understanding or misconceptions.

Here's where reality hits. These aren't simple recall questions testing whether you understand put-call parity or differences between forwards and futures. Though sure, you'll see some straightforward conceptual items. But a significant chunk involves multi-step quantitative problems requiring you to compute bond duration after first finding the yield, then computing cash flows, then properly weighting them. Or binomial option pricing trees where you're working backward through multiple nodes while applying risk-neutral probabilities at each step. That's what separates passing candidates from failing ones.

Time management becomes critical. The exam duration gives what seems like adequate time on paper. Most candidates report finishing with maybe 10-15 minutes for reviewing flagged questions if they're methodical and don't panic. But get stuck trying to derive something from first principles instead of recognizing the pattern? You'll run short fast.

The calculator becomes your best friend. Calculators are permitted and necessary since you're definitely not doing present value calculations or portfolio variance manually. I once watched a guy try to calculate compound interest longhand during a practice session and he was still on question three when everyone else finished. Don't be that guy.

The difficulty level nobody discusses honestly

The PRM Exam I difficulty level occupies interesting middle ground. It's not as brutally full as CFA Level I covering ten topics requiring 300+ hours for most people. The 8006 exam focuses more narrowly on time value of money, portfolio theory, fixed income, derivatives, market structure.

But here's the thing: what it covers, it covers deep. Especially quantitative material. Where FRM Part I might ask you to identify which factor affects option value, PRMIA Exam I expects you to calculate the actual option price using two-period binomial models, adjust for dividends, and explain why early exercise might be optimal for American puts. Different engagement level entirely.

Compared to the 8007 mathematical foundations exam coming next in the PRM sequence, Exam I's less theoretically dense. You're not proving convergence properties or deriving distributions, but you need comfort with algebra, basic calculus concepts (especially for understanding option Greeks like delta and gamma), probability, statistics. If you froze during undergrad stats, you'll struggle.

Common pain points? Option pricing mechanics trip people up constantly because one early calculation error cascades through the entire problem. Fixed income math presents another wall, particularly duration and convexity. Lots of candidates memorize formulas but can't distinguish between Macaulay duration and modified duration or explain why convexity matters for large yield changes. The exam punishes surface-level memorization hard.

How questions actually test your knowledge

Scenario-based items comprise a meaningful portion. You'll get market situations. Maybe a portfolio manager holds bonds expecting rising rates, or a corporate treasurer needs to lock in borrowing costs. Then the question asks you to identify the appropriate hedging strategy, calculate the hedge ratio, or explain what happens if scenarios shift. These integrate multiple concepts at once. You're applying portfolio theory to construct derivative hedges or using arbitrage pricing theory to spot mispriced structured products.

The "except" and "not" questions deserve special mention. They cause stupid mistakes. "All of the following are true EXCEPT" requires finding the one false statement among plausible-sounding options, and under time pressure, candidates miss that word, selecting the first true statement they see. Read carefully. Twice.

Questions incorporate real-world complexity textbooks sometimes gloss over. Accrued interest in bond pricing, dividend adjustments in equity derivatives, day-count conventions differing between instruments. The 2015 Edition doesn't let you live in some frictionless theoretical world. You're handling bid-ask spreads, margin requirements, settlement conventions.

What "passing" actually means for prep

The exam doesn't use negative marking. Wrong answers don't subtract points, so strategic guessing on questions where you've narrowed it to two choices makes mathematical sense. But the passing threshold sits high enough that you can't guess your way through. You need solid mastery.

PRMIA adjusts the passing standard periodically to maintain consistent certification quality as exam forms change, which means you can't rely on "I heard it was 65% last year" as your target. You should aim for 75-80% mastery in practice work, building a safety margin. Because exam-day anxiety, tricky question wording, and the occasional curveball you didn't anticipate all erode performance below your practice level.

Score reports, if you don't pass, typically break down performance by content area. That feedback helps target weaknesses for retakes. But retakes cost money and time, so getting it right initially matters. The 8006 practice exam questions pack at $36.99 gives you question exposure to calibrate your readiness. Not just seeing if you know formulas, but whether you can apply them under realistic conditions.

Blueprint and time allocation strategy

The examination blueprint specifies approximate weights for each content domain. Finance theory foundations might be 30%, financial instruments 40%, markets and pricing 30%. Those aren't exact figures, but it illustrates how you should allocate study time. Don't spend 60% of prep on portfolio theory if it's only 20% of the exam.

Within instruments, derivatives typically carry heavy weight. Options especially. You need comfort with Black-Scholes intuition (even if you're not deriving it), binomial models, put-call parity, Greeks, and how dividends affect everything. Fixed income comes next: bond pricing, yield measures, duration, convexity, term structure. Equities get less attention but you still need CAPM, dividend discount models, market efficiency concepts.

The difficulty balances accessibility with rigor. PRMIA wants motivated candidates with solid finance backgrounds to succeed, but they also want the certification to mean something to employers. If 90% of candidates passed, the credential would lose value. If only 20% passed, people would abandon the program entirely. Historical passing rates suggest something in the 50-65% range for well-prepared candidates. Moderate difficulty. Not a gimme, definitely not impossible.

Calculator proficiency and computational efficiency

You'll be doing present value calculations, bond pricing with semi-annual coupons, option valuation, portfolio variance with correlation matrices, CAPM beta estimation. All requiring calculators. Get comfortable with your calculator's functions before exam day. Know how to chain calculations, use memory functions, work efficiently.

The exam doesn't care if you understand the concept if you can't execute the calculation accurately in three minutes. Practice timed problem sets. Not open-book leisurely working through examples, but closed-book, timed, realistic pressure. That's where 8006 practice materials earn their value, simulating the actual cognitive load.

Conceptual depth requirements

Memorizing that put-call parity's C - P = S - PV(K) isn't enough. You've got to explain why it must hold. Because otherwise arbitrageurs would exploit the mispricing until it corrected. And construct the arbitrage strategy if parity's violated. That deeper understanding separates candidates passing comfortably from those barely scraping by or failing.

Same with duration. Sure, you can plug numbers into formulas, but can you explain why duration approximates price sensitivity to yield changes? Why it's a linear approximation breaking down for large yield shifts? Why convexity matters? The exam tests that conceptual layer through scenario questions and "which statement is true" items where surface knowledge leads you to confident wrong answers.

After you conquer Exam I, the 8008 risk management frameworks exam awaits, building on these foundations with operational risk, credit risk, ALM. But you've got to nail the fundamentals first. No shortcuts there.

PRMIA 8006 Exam Cost, Registration, and Logistics

PRMIA 8006 (PRM Exam I) overview, 2015 edition

PRMIA 8006 Exam I is the first gate in the PRM program, and the 2015 Edition version is basically your "do you speak finance" check. Finance theory. Financial instruments. Financial markets. It's broad, and honestly, that's the entire point.

This exam isn't trying to turn you into a trader overnight or anything crazy like that. It validates that you can read what risk people write, follow the math when it shows up, and not get completely lost when someone casually drops "duration", "forward price", or "discount factor" in the same sentence like it's nothing. It's the kind of baseline that helps if you're moving into market risk, product control, treasury, risk analytics, model validation, or even quant dev adjacent roles where you keep bumping into pricing and market structure.

Some folks take PRM Exam I Finance Theory because they want a cleaner credential path than doing a full degree again. Others do it because their desk expects it. Wait, there's also folks who do it as a personal reset, which I respect.

What it validates day to day

The exam hits PRMIA Exam I Financial Instruments and PRMIA Exam I Financial Markets in a way that feels like "here's the toolkit, now show me you can use it without panicking." Discounting comes up everywhere. So does basic risk return thinking. You'll also see how common products are quoted and priced at a high level.

The practical win? Communication.

You stop being the person who nods in meetings while secretly thinking "wait, why's the futures price higher than spot again?"

PRMIA 8006 exam objectives (what you'll be tested on)

Finance theory foundations are the spine: time value of money, compounding, discounting, and how expected return relates to risk. All that fundamental stuff. This is where candidates who haven't touched spreadsheets since undergrad get humbled fast, because the exam doesn't care about your job title or how senior you think you are.

Financial instruments are next. Cash instruments like bonds and equities, plus derivatives like forwards, futures, options, and swaps. Not every question's calculation heavy, but you do need to be comfortable with payoff logic and basic pricing intuition. The exam likes applied concepts where one wrong sign flips your answer completely.

Market structure is the third bucket: participants, how markets function, why liquidity matters, and how pricing basics show up in different venues. The thing is, people underestimate this section.

Exam-day skills that sneak up on people

You need to read carefully. You need to do quick math without spiraling. And you need to know what the question's actually asking, because PRM certification Exam I objectives are written to test concepts, not just whether you memorized a definition last night while drinking coffee at midnight. I once knew someone who spent two weeks memorizing formulas but couldn't recognize when to actually use them. Failed twice before switching approaches.

PRMIA 8006 exam format and scoring notes

Computer based testing is the normal route now, usually at Prometric or Pearson VUE, and that scheduling flexibility's a lifesaver if you're working full time and can't just vanish for a day. Testing windows exist, so you're picking an available period and then an appointment inside it. Your study plan has to end when the calendar says it ends, not when your motivation magically shows up.

Question style? Mostly multiple choice.

The scoring approach is pass fail, and your score report may include domain level feedback so you know if you were weak in theory versus instruments versus markets.

About PRMIA 8006 passing score, PRMIA doesn't always publish a simple "X% is a pass" number the way some exams do, and that drives people absolutely nuts. I mean, I get it. You want a target, something concrete to aim for. Treat it like you need to be comfortably above "coin flip" across every domain, because limping through one section and hoping another carries you is how retake fees happen.

PRM exam I difficulty level, compared with FRM/CFA

This is opinionated, but whatever. PRM Exam I isn't as deep as CFA Level I in breadth of accounting and ethics. It's not the same vibe as FRM Part I which tends to push harder on risk specific framing. But PRM Exam I difficulty level is real because it's wide and unforgiving if your basics are rusty, like really rusty from years of not touching this stuff. The math isn't insane. The time pressure can be.

You can pass.

You must practice. You need a plan.

PRMIA 8006 cost and registration (the stuff people ignore)

PRMIA 8006 exam cost is a legit investment in your career, and candidates should budget like adults, not like "I'll just put it on a card and hope everything works out somehow." The exam fee usually includes the admin cost of delivering the exam, score reporting, and yes, some portion supports PRMIA's educational resource development. That's why the fee isn't just "pay the test center twenty bucks."

Registration fees can vary by candidate status, like student versus professional. Also by region and timing, like early bird versus standard registration periods. Early registration's the easiest discount you'll ever get, because all you have to do is commit earlier, and the tradeoff is you lock yourself into a timeline that might get messy if work explodes unexpectedly.

PRMIA membership can matter here. Sometimes it's required, sometimes it offers discounts, and either way it becomes part of your budgeting math because membership plus exam can be more than you expected if you only looked at the headline fee. Not gonna lie, I've seen people get surprised by this and then delay the exam for months because they weren't ready for the total bill.

What total cost really looks like

The exam fee isn't the whole bill, which people forget constantly. Total certification cost usually includes PRMIA Exam I study materials, practice tests, maybe a review course, and potentially retake fees if you miss on the first attempt. Add travel if your test center's far. Add a day off work if you're taking it on a weekday. It stacks up quietly.

A few cost line items to plan for:

- Exam registration and any membership requirements (this is the non negotiable chunk, and you should check your exact pricing on PRMIA's site because it changes by region and period, sometimes significantly)

- Practice content like the 8006 Practice Exam Questions Pack at $36.99, which's cheap compared to a course. Honestly it's useful if you need reps, error logs, and pattern recognition more than another 200 pages of reading that you'll skim anyway

- Retakes, rescheduling, and late fees if things go sideways

- Travel, printing, extra calculator, childcare, whatever your life needs because everyone's situation's different

Employer sponsorship? Worth asking about.

A lot of companies'll reimburse, but only if you follow their process, like pre approval, proof of pass, or using a corporate card instead of personal funds. Tax deductibility's also a thing in some jurisdictions, but talk to a tax pro, because the rules are personal and change a lot depending where you live.

Rescheduling, cancellation, refunds (read this before you click pay)

Rescheduling considerations are where people get burned, honestly. There're usually deadlines, fees for date changes, and sometimes blackout periods when you can't move appointments at all. Pretty frustrating. That matters because rescheduling also messes with your study momentum, and if you push it two weeks you might feel relief for one day and then spend the next thirteen days half studying and half doom scrolling through finance Twitter.

Cancellation and rescheduling policies typically set a cutoff. Miss it and you pay, simple as that. Refund policies are usually tight, with refunds limited to documented emergencies or PRMIA initiated cancellations. If you no show, you usually forfeit the whole fee with no credit. Harsh? Yes. Standard? Also yes.

Retake fees apply if you fail, and some places require waiting periods between attempts, so you can't always just rebook next weekend and try again immediately. Some people want to do that out of frustration.

Plan your first attempt like you don't want to pay twice.

Logistics: test centers, ID, rules, calculators

Computer based testing at Prometric or Pearson VUE is convenient, but geographic availability matters a lot. If you live in a major city, cool, you've got options. If you're remote, you might be driving a few hours or booking a hotel, and suddenly your PRMIA 8006 exam cost includes gas and a room, maybe even meals if you're making a weekend of it.

After registration, you'll get a confirmation with your test center, reporting time, and identification requirements that you need to follow exactly. Your ID needs to match your registration name exactly, usually a government issued photo ID. If your profile says "Mike" and your passport says "Michael", fix it early, don't gamble on them being flexible.

Testing center rules? Strict.

No phones. No watches. No notes. Bags go in secure storage. Scratch paper's provided and collected after, because exam security's serious and they're not messing around.

Calculator rules matter too, more than people think. PRMIA typically allows financial or scientific calculators without communication features, but you should confirm the current list before exam day because it changes sometimes. Show up with an approved calculator and fresh batteries. Small thing. Big stress reducer.

Accommodation requests for disabilities are possible, but you need to do it early with documentation so PRMIA can arrange reasonable modifications and actually have time to process everything. Waiting until the week before's how you end up taking the standard session anyway.

Results and what happens after

Results are usually delivered electronically within a specified timeframe after exam administration. Not immediately which some people expect for some reason. Score reports typically show pass fail and may include performance feedback by content domain. That's helpful for planning a retake or just understanding where you were strong versus where you got lucky.

Passing candidates get a digital certificate and authorization to use the PRM Exam I designation, which's the whole point. Failing candidates get guidance on retake procedures, possible waiting periods, and which areas need work based on their performance breakdown. If you fail, don't just reread everything hoping it'll click. Use a question bank, track mistakes, and fix the gaps systematically.

That's also where something like the 8006 Practice Exam Questions Pack can fit, because drilling PRMIA 8006 practice tests and keeping an error log's often more effective than doing another full read through when the issue's application, not exposure to the material.

Practice tests and study materials that actually help

Official readings are the base. Start there, no shortcuts. Add supplementary notes if you need clarity, but don't collect resources like trading cards where you've got seventeen books and finished none of them.

Pick a set. Finish it.

For PRMIA 8006 question bank style prep, do timed sets early, not just at the end, because timing's a skill you develop gradually. My favorite method's one long rambling routine where you do 25 questions timed, review every miss and every lucky guess, write a one line rule for each concept you got wrong, then redo those questions a week later to prove you learned it instead of just recognizing it from short term memory.

Benchmarks matter here. If you're consistently scoring well on mixed topic mocks, you're close to ready. If you're only scoring well when you cherry pick topics, you're not ready yet, period.

If you want a lightweight add on that won't blow your budget, the 8006 Practice Exam Questions Pack is priced at $36.99, and it's an easy way to add volume without signing up for a full course that costs ten times more.

quick FAQ style answers people ask anyway

What's PRMIA 8006 and what does it cover? Finance theory, instruments, and markets, aligned to the Professional Risk Manager Exam I syllabus for the 2015 Edition.

How much does the PRMIA Exam I cost? It depends on membership, region, and timing, and you should budget for extras like study materials and rescheduling fees just in case.

What's the passing score for PRM Exam I? PRMIA may not present it as a single fixed percent, so treat your goal as strong performance across domains, not squeaking by in one and bombing another.

Best study materials and practice tests? Start with official readings, then add targeted question practice, ideally timed, with a small set of resources you actually complete instead of hoarding.

Prerequisites, Recommended Background, and Candidate Preparation

Look, PRMIA deliberately keeps the entry barriers low for the 8006 exam. There's no hard wall stopping you from registering. No degree requirement, no previous certification, no mandatory three years in finance. You can sign up tomorrow if you want. But honestly, that accessibility is kind of deceptive because the exam itself assumes you already know quite a bit. The gap between "can I register?" and "will I pass?" depends almost entirely on what you're bringing to the table.

The gap between eligibility and readiness

PRMIA doesn't gate-keep registration, but they absolutely expect undergraduate-level competence in finance, economics, and math. If you've got a finance degree or something close (economics, business with a finance concentration), you're starting from a much better position. The exam doesn't spend time teaching you what a bond is or why discounting matters. It assumes you've seen corporate finance, investments, maybe a derivatives course. Candidates without that foundation? They're not blocked from attempting it. But they're signing up for a much longer, steeper climb.

I mean the recommended coursework isn't exotic. Corporate finance gives you time value of money, capital budgeting, basic valuation. Investments covers portfolio theory, asset pricing, market efficiency. Derivatives gets you into options, futures, swaps. The instruments that trip up a lot of people. Financial markets and institutions provides context on how everything fits together, who the players are, why markets behave the way they do. Statistics underpins the risk measurement side. You don't need all of these, but each one you're missing adds weeks to your prep timeline.

Math matters more

The mathematical prerequisites aren't brutal, but they're real. You need solid algebra. Rearranging formulas, solving for unknowns, working with exponents and logarithms. Basic calculus comes up, especially conceptually. You don't have to compute complex integrals by hand, but you should understand what a derivative represents (rate of change) and what an integral does (accumulation). This matters because option Greeks are literally derivatives. Delta is the first derivative of option price with respect to underlying price, gamma is the second derivative. If calculus is completely foreign to you, those concepts become memorization instead of understanding.

Probability theory and statistics? Absolutely foundational. Mean, variance, standard deviation. These aren't just formulas to memorize, they're the language of risk. Correlation, covariance, regression analysis all show up in portfolio theory and factor models. Probability distributions (normal, lognormal, binomial) underpin option pricing and risk calculations. If your stats background is shaky, you'll struggle with large chunks of the PRM Exam I Finance Theory material. Not gonna lie, candidates who took a decent probability and stats sequence have a real advantage here.

Linear algebra helps with portfolio optimization and multi-factor models. Understanding matrix operations, solving systems of equations. The thing is, it's not absolutely required for Exam I. You can get by without deep linear algebra knowledge, though it makes certain topics click faster if you have it.

Tools you should know

Financial calculators are basically mandatory. The HP 12C or BA II Plus. Pick one, learn it thoroughly. Time value of money calculations, bond pricing, yield measures, amortization schedules. You'll solve practice problems much faster if you're fluent with your calculator rather than fumbling through the manual every time.

Excel proficiency is less critical for exam day but incredibly useful during prep, honestly. Building your own bond pricing model or option payoff diagram in a spreadsheet cements understanding in ways that passive reading never will. I spent a weekend once just modeling different volatility scenarios for call options. Sounds tedious, but watching those Greeks shift around gave me more insight than any textbook chapter.

Experience changes everything

Prior exposure to financial markets? Total big deal. Work experience in trading, risk, banking, asset management means you've seen these concepts in action. A derivatives trader might not have formalized the Black-Scholes math, but they intuitively understand how delta hedging works. Someone from credit analysis has wrestled with financial statements and default risk. Even personal investing or following markets seriously gives you vocabulary and context. Abstract theory becomes concrete when you can connect it to real market behavior you've observed.

Accounting knowledge helps more than you'd expect. Understanding balance sheets, income statements, cash flow statements supports equity valuation topics, credit analysis, and financial statement interpretation. You don't need to be a CPA, but basic accounting literacy matters. Knowing what retained earnings means, how depreciation works, why cash flow differs from net income. This makes several exam sections much less mysterious.

Different backgrounds create different challenges

Candidates from quantitative fields (math, physics, engineering, computer science) usually crush the computational aspects. They're comfortable with formulas, probability, optimization. But they sometimes lack market intuition. They can derive the put-call parity relationship but don't instinctively feel why a deeply out-of-the-money option trades near zero. Building that intuition requires reading financial news, following markets, understanding why prices move the way they do.

Traders and banking professionals bring the opposite profile. Tons of practical knowledge, maybe weaker theoretical foundation. They've executed swaps but might not have formally studied no-arbitrage pricing. They know credit spreads widen in crises but haven't worked through the mathematical relationship between default probability and bond yields. For them, the PRMIA Exam I Financial Instruments challenge is formalizing and systematizing what they already know intuitively, plus filling theoretical gaps.

Recent graduates? Current academic knowledge but limited real-world context. They can recite CAPM but haven't watched a market crash unfold. They understand option payoff diagrams but haven't felt the pain of gamma risk in a volatile market. Reading the Wall Street Journal, Financial Times, or Bloomberg regularly helps bridge that gap. Understanding the 2008 financial crisis, the European debt crisis, why certain regulations exist. This context explains why the exam emphasizes particular topics.

Calibrating your timeline

If you've got a finance degree, took derivatives and investments courses, work in a related field, and your stats is decent? Maybe 150-200 hours of focused study gets you there. That's three to four months at 10-12 hours per week. Without that background? Double it. Seriously. You're not just learning exam material, you're building foundational knowledge that other candidates already have.

Candidates without formal finance education should budget extra time for foundational concepts before even touching PRM certification Exam I objectives directly. Maybe work through a corporate finance textbook first, then an investments book, then approach the official PRMIA material. It's frustrating but necessary. Jumping straight into exam prep without those foundations leads to memorization without understanding, which crumbles under exam pressure.

Regulatory and market awareness

Understanding the regulatory environment isn't explicitly tested much, but it provides essential context. Why do Basel accords matter? What role do central banks play? How do clearing houses reduce counterparty risk? Recent financial crises (the 2008 meltdown, flash crashes, sovereign debt issues) aren't just history, they're case studies explaining why risk management exists and why certain instruments and practices get scrutiny.

The more you understand about market structure, participants, and mechanics, the easier abstract concepts become. Knowing that market makers provide liquidity but face inventory risk helps you understand bid-ask spreads and dealer hedging. Recognizing that pension funds have long-duration liabilities explains their bond portfolios and interest rate sensitivity. This awareness doesn't come from textbooks alone. It comes from reading, following markets, and paying attention to why things happen.

Reality check time

The 8007 (Exam II: Mathematical Foundations of Risk Measurement) is generally considered more quantitatively intense, but Exam I still filters out unprepared candidates. The breadth is challenging. You need competence across finance theory, fixed income, equities, derivatives, and market structure. Depth matters too. Superficial understanding doesn't cut it when questions test application and interpretation, not just recall.

Compared to FRM or CFA? Exam I is narrower in scope but assumes similar foundational knowledge. It's not easier, just different focus. Wait, actually I'd argue it's more concentrated, which makes weak spots harder to hide. Candidates who underestimate it because PRMIA doesn't require prerequisites often regret that assumption after their first attempt.

The bottom line? You can register without prerequisites, but you can't pass without preparation that assumes significant background. Assess honestly where you stand. Budget your study time accordingly. Build foundations before diving into advanced material. The exam doesn't care whether you learned this stuff in school, at work, or self-study. It just expects you to know it.

Conclusion

Wrapping it all up

Here's the deal. The PRMIA 8006 Exam I? You can't cram this thing the night before and hope it magically works out. I mean, it tests finance theory, financial instruments, and financial markets at a depth that really expects you to understand how concepts connect to each other, not just regurgitate formulas you memorized an hour ago. You need a legit study plan. One that actually gives you enough runway to wrestle with derivatives pricing, nail down fixed income math, and get really comfortable with market structures before you even consider booking your exam date.

The PRMIA 8006 exam cost and logistics? Pretty straightforward. You pay. You schedule. You sit. But the passing score is where reality hits most candidates square in the face and they realize this certification isn't some participation trophy deal. PRMIA sets the bar intentionally high because the Professional Risk Manager certification carries real weight in risk management circles. You don't wanna show up half-prepared and hemorrhage money on retake fees just because you skipped practice problems or glossed over the gnarlier sections of the PRM Exam I Finance Theory material.

The biggest mistake? People lean exclusively on official readings without actually testing themselves nearly enough. PRMIA Exam I study materials are critical, sure, but if you're not grinding through PRMIA 8006 practice tests on the regular, you won't identify your weak spots until it's way too late. Like, sitting-in-the-exam-center too late. Mock exams reveal how questions get worded, what time pressure actually feels like, and which topics you thought you understood but.. wait, do I really get duration vs. convexity?

The PRM Exam I difficulty level isn't ridiculous. It's totally passable. But only when you've encountered enough question variations to spot patterns and sidestep beginner mistakes. I remember my brother spent three weeks just on option pricing models because he kept mixing up the assumptions. Tangent, but it shows how one weak area can spiral if you don't catch it early.

And after you pass? You're not finished. Not even close. The PRM certification path keeps going with additional exams, plus PRMIA recertification requirements mean you'll be keeping current with continuing education down the road. But that first exam, the 8006, becomes your foundation. Nail it and everything that follows gets considerably more manageable.

Want a serious edge? The 8006 Practice Exam Questions Pack is absolutely worth your time. Real question formats, thorough explanations, the kind of repetition that really builds confidence instead of false hope. Not gonna lie, practice questions transform "I think I know this" into "I've got this." Give yourself that advantage.